Figure out how to get out of debt with these steps, and start living the better life you dream about. The #yearofno technique is what you need to succeed this time!

The notepad in front of us clearly wasn’t lying.

We were up to our eyeballs in debt.

Again.

And that meant that all the plans we had just made for our upcoming year clearly weren’t happening.

Something had to give.

Debt was ruining our lives. And we were finally ready to do something about it.

But what made this time different?

Well, that’s what surprised us the most.

How The Heck To Get Out of Debt When Nothing Has Worked So Far

The Most Important Thing That You MUST Do First

I know everyone tells you that the first thing to do is to figure out how much debt you have, or to make a list of who you owe.

But don’t do that.

You’ll be missing out on the absolute most crucial step.

Because the very first thing you need is a good “why”.

This “why” is going to mean EVERYTHING to you. You’ll cling to it for months (or years) while you pay off debt.

Like Curly from City Slickers, I can’t tell you your why. Only you know that.

Before you click play…language warning!

So dig deep and figure out why your family needs to escape credit cards, car payments, student loans, or whatever bills you hope to lose.

Your why can be big or small, but it must be significant to you.

- So your kids don’t repeat your mistakes.

- To take that dream vacation

- Because you want to move to a better home.

- You want to stop being afraid to check the mail.

- So sleep becomes your friend again.

Once you know your why, cling to it. Make it your mantra.

What worked for us?

Well, we lived in a house with one bathroom for seven people. We really wanted a second bathroom.

(And today, we actually have one!!)

Rule #2: Learn The Best Way to Pay Off Debt

Now that you know your why, figure out your how. What debts do you have?

If you aren’t sure exactly what money you owe, follow the same steps I took when I learned how to find out all my debts.

Write down all of them, and pay attention to how they make you feel. You’ll need passion to get you through the first pay off.

Some Good Options

1. Use That Anger For Good!

This was the clear winner for us.

Instead of worrying about paying off the guy we owed the most or the smallest amount to, we focused on passion.

There was one card that always made me angry. The company wasn’t very nice, and the money sitting on that card had been spent on stupid things.

It was pure pleasure to make the last payment on that card.

And that kept me going when it was hard.

So which debt makes you feel the strongest emotions? Maybe there’s one bill that makes you angry. Or a company that has been extra annoying.

Get rid of them first.

2. Embrace Your Inner Nerd

Tackling the highest interest rate first makes the most sense mathematically. But if you don’t feel passionate about paying that debt, you’ll quit before you really begin.

So in the long run, it’s most important to choose the card with the strongest mental win for yourself.

You’ll need that emotional high to power you through.

(After all, saving money on the interest rate will do you no good if you don’t follow through with the plan!)

3. Go Big

Choose to pay the biggest debt first.

If you get rid of that beast, you can do anything. I call this the “king of the world” option.

Rule #3: Find the Cash

Most of us have more money than we think.

Get ready for the ugly stuff…

The hard truth is that if you spend money at a drive thru, on a dozen subscriptions, potato chips, or fancy clothing, then you have money to pay off debt.

We used some free budgeting apps to help us find out what we were spending all of our money on.

But honestly, the free apps kept going under or getting sold. And how many different companies do you want to give access to your money?

These days we use the Every Dollar app from Dave Ramsey. Even though we pay for it, it’s saved us way more than enough to cover that cost. Plus, if you use this link you’ll get $10 off the price! (Whoop, whoop!)

Plus it makes building a budget a lot more fun than trying it with paper and pencil like we did back in the 1900s.

Rule #4 What’s A Motto With You?

We didn’t understand the power of having a motto…until one found us.

You see, we didn’t actually set out to pay off a bunch of debt.

No, we were in the process of making a bunch of plans to fix things around the house, go on vacation, and hoping to do some “dream big” stuff with our kids.

But when we looked at our budget, we realized that none of that was really possible.

Because our credit card payments were eating all that money we wanted to spend on more fun things.

Yikes!

So my husband crossed everything off our list of fun. Instead, he wrote across the top of the paper… #yearofno.

And our motto was born.

It got us through some really tough times!

And it meant we didn’t have to justify things or explain anything. #Yearofno became a complete sentence.

What Did Our #YearofNo Look Like?

Don’t confuse the #yearofno with a spending freeze.

You might get through a spending freeze for a week or even a month (by the skin of your teeth).

But most people just hold their breath through the freeze and buy the things they wanted once the freeze is over.

That does nothing but delay spending.

Instead, #yearofno makes lasting changes. It’s all about knowing the difference between need and want.

Our family refused to buy any extras at all for an entire year.

That meant no book fairs, no fast food, no drinks from the concession stand, no replacement furniture, nothing.

We forced ourselves to use it up, wear it out, make it do, or do without.

A #yearofno will retrain your brain. It’s as easy as this: the answer to any spending starts with a strong no. To actually spend the money, you’ll have to convince yourself that there is no other way around it.

- Do we absolutely need this for good health and well being? (Food, shelter, necessary clothing)

- Will putting off this purchase mean we’ll spend more than double or triple the cost in the long run? (Home and car repairs and maintenance)

- Is this a once in a lifetime opportunity… that I can pay cash for? (Like that fifth grade only special field trip or a First Communion.)

And here’s a helpful clue: If you have to speak more than one simple sentence to justify a purchase to yourself, you don’t need it.

Rule #5: Work for It

If you’ve already been living this way and you still have no money to pay off debt, you’ll need to get a second job.

The good news about taking on extra work is that you’ll have even less time for spending money!

Here’s a whole list of work from home jobs you can try to earn some extra money.

Rule #6: Beat The Clock

(Maybe this one isn’t so much a rule, but it makes it more fun.)

This one is perfect for people who get excited when they beat the time Waze gave them to get to a destination.

Anxious to get out of debt faster? Sell everything you own that isn’t essential to living a good, healthy life.

If your car payment is too high, then save up (#yearofno) or work side jobs until you can pay the difference between what it’s worth and what you owe.

THEN…sell the car and buy a more reasonable vehicle.

Want to earn some extra money to pay it off even faster? Think of dirty jobs that others don’t want to do.

Mike Rowe’s advice is spot on, whether you’re looking for work that pays better or just want to get a raise or promotion doing what you already love.

Remember that if you’ve been “charging it” for years, there’s no magic bullet for getting out of debt quickly. But if you start today, you’ll be finished that much sooner.

One Last Thing

Pulling together an emergency fund when you should be paying every extra dollar on debt feels counterproductive.

But here’s why it isn’t.

At the same time you’re paying off debt, you need to teach yourself how to live without credit cards.

Your car doesn’t care that you’re paying off debt. It’s going to break down anyway.

Your washer doesn’t care about your goals. It’s going to fritz out when you least expect it.

Having a small emergency fund will teach you how to rely on yourself when you need to buy something unexpected.

You’ll need the confidence boost you’ll get from saying things like, “Hey! I paid for that repair myself!”

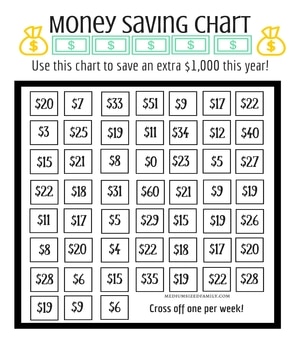

Use my 52 week money challenge to help you pull together $1,000. But instead of taking 52 weeks, challenge yourself to find those bits of money in the shortest time period possible.

Then you can start your debt payments ASAP.

That’s How To Get Out of Debt!

Getting yourself out of debt is important, so don’t let someone else do it for you. Not only will you get the benefit of fewer bills, but you’ll also give yourself a PhD in Money Management. That will serve you for a lifetime.

Have you successfully paid off debt? How did you do it?

“Debt is the “loading” bar that will never let you see the entire video. If you’re tired of waiting for life to get to the good part, you have to learn how to get out of debt.”

Perhaps the best explanation I’ve ever read on why it’s critical to get out of debt. Thank you, Jamie. And your #yearofno strategy is pretty awesome too. Find your why, follow the three #yearofno spending rules, and crush your debt. I love it.

Wow, thank you so much! I’m living it, so I know that’s exactly how debt feels. The #yearofno has been effective for us, and I hope it helps others, too!

That is one of the best posts I have read to pay off debt or to keep out of debt. Don’t buy what you don’t need. Use your stuff until it wears out. Don’t always being looking to upgrade to the newest thing that marketers are promoting. Don’t try to never spend because that will just lead to a bindge. Find a healthy balance and learn how to spend wisely.

Exactly! Our #yearofno has certainly taught us what’s most important in life.

Great post, Jamie! I completely agree that reducing debt takes passion. We’re passionate about debt reduction because we’re so tired of living with that weight on our shoulders. It’s holding us back. Plus, we’d love to be able to buy our own home.

I’ve found that my anger and frustration over living in the shadow of debt has gotten me over a few very difficult months when we were just sick and tired of the whole fight. I know you’ll get that home!

This is a really great post, Jamie! I’ve been doing an informal “6 months of no” for the last six months and… I’m actually a lot happier because of it! Is that weird? I’m really happy I’ve actually been able to save more and, sure, I don’t go out with friends as much as I did before, but I have SAVINGS at the end of the month! It’s a miracle! 🙂

A year of no would be difficult but I think a year of concentrated, informed no is good. I won’t be able to say no to everything (nor would I want to!) but making an informed no based on my budget is definitely possible 🙂

I found that the entire solid year of no reset us. Our second year hasn’t been as strict as the first year, but the new mindset we have makes it a lot easier.

I love the idea of your #yearofno. You’re absolutely right that you need to retrain your brain to make lasting changes. Even just starting to ask yourself questions each time you go to spend can help you to focus on your needs rather than your wants. And you’ve provided a great example to inspire others to get out of debt.

Thank you! It’s definitely made a lasting change in our family.

Nice job getting on Rockstar Finance, Jamie! Solid article!

Thank you!