A sinking fund is the only thing standing between you and freedom from paycheck to paycheck living. Here’s how to get started.

Watching the balance on our biggest credit card shrink over the past year has been…how should I put this?

Ah-maz-ing!

Our main goal in our #yearofno has been to knock out debt every chance we get.

Read all how we’re getting out of debt here (yes, even while raising 5 kids on one income!).

But there is one thing that I wish we had done differently.

Something that could have made a bigger difference in our debt payments.

It’s called a sinking fund. It’s a genius (but uncomplicated) idea that prepares you for those nagging expenses that add to debt.

Everything You Need To Know About Sinking Funds

What is a sinking fund? How can you get one? Why should you get one?

This is gonna change your life in a fantastic way!

A Sinking Fund Is NOT An Emergency Fund

Emergency funds are important, of course.

But a sinking fund… is not your emergency fund.

You see, emergency funds are good for covering expenses that come out of nowhere and can bankrupt you in no time.

Things like a sudden layoff, an accident, or a surprising health discovery are emergencies…those are reasons to raid your emergency fund.

BUT, those bills that you know are coming, but they don’t happen regularly enough to really plan for them? You don’t really want to use your emergency fund for those things.

You kinda lost track of the last time you bought tires, and before you know it, someone points out that they’re looking pretty worn out.

That video game your oldest has been practically drooling over is finally on sale. You’d love to get it for his birthday in a couple of weeks.

Those are the kind of things that will make the sinking fund your hero.

Ok, What Is A Sinking Fund?

Sinking funds are money you keep in an account (or a set of envelopes) that’s just for specific expenses that pop up and give you a headache.

- Once-a-year insurance bills.

- Unpredictable car repairs for your 10 year old car.

- Garbage bills that get paid every 3 months (but you can never remember exactly which month they’re due).

When those bills come in the mail, do you get a sense of dread in the pit of your stomach?

Maybe you can cover this bill, but it will be a stretch.

Or worse, it’s going to have to go on a credit card (again).

The job of a sinking fund is to keep that sinking sensation away.

Once you get yours together, you’ll open that bill and know right away that you have the money to cover it.

How to Set Up Your Sinking Fund

Setting up a sinking fund can be done in a couple of ways.

One simple way is to have envelopes in a drawer somewhere labeled with what you’re saving for.

But these days, our family prefers to keep our money in a bank account. (Specifically an online account that’s easy peasy to use.)

While our regular checking account is held at a brick and mortar bank, we like to store our sinking funds accounts online.

That’s because there are so many options there for free checking or savings accounts. And many online banks can offer a higher interest rate.

It used to be that ING Direct was the best deal out there, but that morphed into Capital One 360. (I know that sounds like a credit card, but it really is an online bank.)

We’ve also used Ally Bank online, and have looked into Discover Bank. There are plenty of good options out there.

Whatever new account you open, the best reason to open a separate account is as simple as “out of sight, out of mind”.

Put your sinking fund money in account you don’t access regularly, and it won’t “accidentally” get spent as easily.

You can keep a debit card for this account, or you can just set up online bill pay.

Avoid ATM fees by doing a cash advance on your debit card inside your local bank.

Sinking Fund Examples

The next thing to do is list everything that deserves a line in your sinking fund.

You might not have the money to fund it all yet, but you should still list all the categories you can think of. (Yes, even that dream vacation to the Caribbean.)

Some sinking fund category suggestions include:

- bills that don’t get paid monthly, like trash or water

- car taxes or tags

- insurance bills

- Christmas

- vacation

- school or membership fees

- kid’s sports or activity fees

- summer camp

- car repair and maintenance (including tires and oil changes)

- birthday gifts

- home maintenance

- appliance repair or replacement

- healthcare copays (though you’re better off getting tax breaks on an FSA or HSA)

- big expenses you are expecting soon such as braces or furniture replacement

- extra reindeer food in December 😉

- think through the months of the year and what random expenses seem to pop up

Sinking Fund Calculation

Next, let’s to talk numbers. (Math haters, I’m right there with you! Just pull out your trusty calculator…this won’t be too painful!)

Next to each category you wrote in that last step, determine how much money you spend on that item per year.

Some will be straightforward.

Bills that usually stay the same price, but don’t come every month are an easy way to start. (Looking at you again, garbage bill.)

Others are more elusive.

How long has it been since you bought tires?

How often do you get oil changes?

If you use a debit or credit card for these things, you can search your statements to get a better idea. Otherwise, an educated guess is good enough.

The goal is to get it set up. You can tweak it as you go.

Done is better than perfect!

If this seems complicated, a free Personal Capital account might be just what you need to figure out your numbers!

Don’t Freak Out!

You might notice that the numbers are climbing.

Maybe they even exceed any amount you could ever hope to keep up with.

Don’t give up hope yet!

Put your items in order from most important to least important. Fund as many accounts as you can before the money runs out.

Filling the vacation and Christmas funds is more fun, sure, but a having a reliable vehicle should probably come first.

Remember, though, that the fun stuff should still earn a place on your chart. Once you get ahead, you’ll be able to fill them, too.

The Math Part

Now you’ve written a yearly amount down for each category, so divide that number by 12.

That’s how much money you’ll need to put into the account every month to keep up with these expenses.

If you get paid biweekly and want to divide it by 26 so you can pay from each check, do that.

You might also use bonuses, tax refunds, extra paychecks, or pull in some extra money by doing a work from home job every once in a while.

Now go down the list and see how many categories you can fill with the amount of money you can afford from your monthly budget.

If you don’t like what you’re seeing, be sure your categories are in order. Most important items at the top.

Don’t get discouraged!

How To Track Your Money

If you are using envelopes, this part is easy. Just write one category on each envelope and drop the right amount of money into each one.

On the other hand, if you’re dumping it all into one bank account…it’ll be a little different.

But it’s not hard.

Get a spiral notebook or set up a spreadsheet to record your categories. Use one page for each category.

Just write the category at the top.

Then, whenever you deposit money, mark down how much you put into each category.

If you deposit $50, make sure you write an amount on each page to show how you want that $50 broken down.

How do you decide the breakdown? Well…

- You might decide that the first category is the most important, and you want to fill it as fast as possible. So you’ll put all of your money into that page.

- Or you may decide that the first 3 categories are all pretty important. So you’ll divide the money you have available into thirds, and put one chunk into each of the categories.

- You could even decide to put half the money into the first category and divide the rest equally into your other categories.

You know your situation best. You’ll have to decide how to layer your money to match your situation.

As you spend from this fund, write down any expenses on the page they belong to.

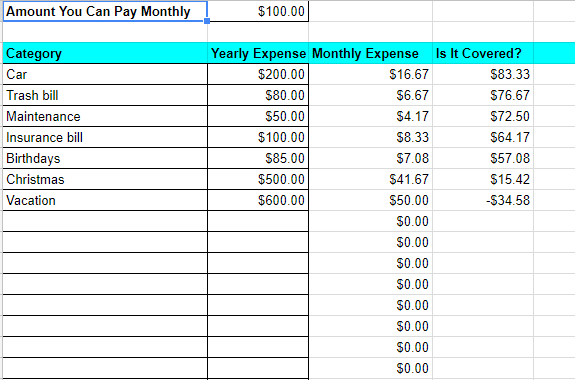

A Free Sinking Fund Spreadsheet

If you prefer a good spreadsheet (Me! Like the proud nerd I am.) I’ve put one together for you.

You can access this in Google Sheets (similar to Google Docs).

Click here or on the sheet below, make a copy, and save it as your own.

You can move around your own categories. Simply put in the amount you can afford monthly.

Type in your categories and how much each of them cost per year.

The sheet will take care of the rest of the math.

Play with it a bit until you’ve filled as many important funds as possible.

- Can you do without anything?

- Is there a way to increase your monthly amount?

Click the spreadsheet below to save your own copy of the sinking fund spreadsheet! (Go to File and choose Make a Copy.)

Where To Find the Money For Sinking Funds

If you can’t find the money in your monthly budget, try to fill this fund with extra money you find.

You might want to use an “extra” paycheck you get in a month of 3 paydays.

Sinking funds can seriously change your future…for the better!

You’re going to love the feeling of confidence you feel with the next irregular bill!

Have you ever saved up for expenses like this?

![]()

Neat way of looking at it, Jamie. There are certainly costs that aren’t regularly but can be anticipated and funded from regular income. We usually just maintain a buffer in our regular account for them, but having a dedicated fund to move the money out as you earn it makes a lot of sense…that way you have it when you need it.

Ohhh, I feel a spreadsheet session coming on! I am like you – I love me some Excel for budgeting. I had a decent idea what a sinking fund was but this is a way more clear path to pursue. Thanks!

Great budgeting ideas and plans. Pinned.

I hate the feeling of not having enough money when unexpected bills arrive. I do have a sinking fund, although I’ve never called it that. It definitely helps to reduce the stress when there are unexpected expenses.

I’ve never heard of a sinking fund before, but it sounds like a great idea, especially if you’re trying to get out of debt or stop living paycheck to paycheck. I know you mentioned a Capital One 360 checking account for your sinking fund, but if you put it into one of their savings accounts, you could separate it out into the various categories, and simply transfer the amount into your main checking when needed. Either way, it sounds like a great way to be prepared for all the different expenses that pop up.

Great way of budgeting! My husband is our budgeting genius! 🙂 I am pretty darn thankful for that. We use separate accounts to keep track of our money. Thanks for sharing your genius Ideas. #FridayFrivolity

Jamie, I am pinning all of your financial post for future use. I have heard of a sinking fund before but did not know what it was. These are the things and that end up sinking us! As soon as Levi is able to come home, we will be able to free up about $800 a month, we definitely need to work on this. And your articles will be invaluable towards our goal of alleviating debt. Thanks so much for sharing all your knowledge and experience. I’m sure it helps many more than just me.

You’re so sweet! I know this would help you, and I know just what you mean by those things sinking us!

I’ve been doing this without realizing it with my power bill! When I bought my house, I learned the power, garbage, sewer and water were all on the same bill, and they only come once every two months. Ouch. I started putting $200 every month into a separate account with scheduled transfers from my checking. I forgot for Oct and Nov and couldn’t figure out why that account balance is so low. Luckily I remembered last night when I reviewed the bill. Those expenses can come out of no where, and if I don’t set them aside, I’ll definitely spend them on something else!

I do this???? but never knew it had a name. I actually started it for my two biggest (most painful) expenses, those being property taxes and insurance. Not exactly little bills. From there I began putting in for other irregulars. I will be so curious to see what you share. It has helped me tremendously. You are so good a walking folks through things and encouraging us when it seems to be falling apart. I know it will be a fabulous challenge. Looking forward to it.

Wow, thanks so much for this kind comment. What a great start to my day. 🙂 I’m excited about the challenge, too!

I too have been doing this but never knew it was the sinking fund method. I do it a bit different though. I simply create a spreadsheet for the entire year by month. It sounds like a lot but it’s not (think cut and paste). I start out with my fixed monthly bills. Once I do that I go back and add the expenses specific to that month. For example, February for our family has four birthdays, Sportsman license in March, you get the idea. That way you are automatically funding through your budeting that additional expense that comes first. It takes the stress out of these irregular payments.

This is a great idea – it would be a big help with our energy bills which we pay quarterly. Thanks so much for sharing over at Friday Frivolity!

I’m still giggling over the extra reindeer food! Great tips, as always, Jaime, and I hope you all had a fabulous Christmas! #FridayFrivolity

I have been trying to keep a sinking fund. I am new at budgeting and sinking funds and have looked all over the internet trying to understand exactly how to handle the sinking funds along with my budget. When paying a bill out of my sinking funds, do you not apply the payment transaction to your budget? The fixed transactions are on there. Do you just pay the bill out of SF and not apply to your budget somewhere. This is very confusing to me, please help! Thanks!

In our case, we’d write a line item in the budget for sinking funds money. So if I can afford to move $40 from each paycheck into our sinking funds account, I would have a $40 line item in our budget that says “This money is promised to the sinking funds. Don’t use it for anything else.”

Then when I need to use some money from the sinking funds budget, I DON’T write that in my budget, because I already accounted for it when we first moved that money out of our checking account. Instead, I like keep an entirely separate list of expenses I pull from the sinking funds. You can track that money using the contingency fund spreadsheet I shared above, or you can pull out a tablet of paper and just write down notes of what money has come in our out of that fund.

Make sure you’re putting your contingency fund into a separate account from your budgeting money so you don’t get it all confused!

I hope this helps! Happy to answer any other questions. 🙂

This was so helpful! I am excited to try it!