Wondering how to pay off debt and save money? You can do both, and it will change your life for the better! Take these steps to get it done.

We were running late for school. I hustled the kids to the car (“Tie your shoes in the van!”), slammed the door, jumped in, and turned the key.

The tire light came on.

Should I get out and look? That stupid light comes on all the time, and it’s always just a little low on air. I don’t have time for that.

But I knew it would nag at me all the way down the road. So I jumped out to ease my mind before we rushed to school.

Except that this time, I had a totally flat tire.

Unexpected? Check.

Expensive? Check.

Unexpected expenses are called that for a reason. They pop up out of the blue, and they are never a cheap fix. In fact, they are so likely to happen that they should be expected.

Even if you’re living debt free, most of us are just one or two unexpected expenses away from falling into debt. And if you already owe money, unexpected expenses can put you into a never-ending cycle of bills.

But what if you’re actively paying off debt? Should you really be worried about saving money when you have high interest rates?

How to Pay Off Debt and Save Money

The truth is, that you can’t pay off debt without saving money, but you can’t really save money without paying off debt.

Confused?

Why Your Lack of Emergency Fund Is Keeping You In Debt

1. You Keep Putting Emergencies on Your Credit Card

Each time an unusual bill pops up, we’re tempted to just throw it on the credit card and deal with it later. But before you know it, there’s another expense and you still haven’t paid off the first one.

2. You Don’t Have a Budget

Now, if you keep getting hit with bills you weren’t prepared for, it’s usually a sign that you have no budget. Or the one you’re using isn’t working.

It’s time to look at it again and find a way to add another line item for an emergency fund.

(Get budgeting help here! See the box below…)

3. You Panic-And Then You Spend More

An unexpected bill can cause you to give up on your spending plan altogether. “If I’m going to put this on the credit card, I might as well treat myself to that while I’m at it.”

That attitude will keep you in debt forever.

4. You Don’t Expect the Unexpected

We don’t know when certain expenses are going to hit, or what they will look like. But you can bet your boots that unexpected events are coming.

This is why Grandma told you to save up a rainy day fund.

Get more frugal living tips from Grandma!

View this post on Instagram

What’s the fix?

When you have an emergency in your life, the last thing you need to worry about is how you will pay for it.

A serious problem needs all of your attention, and most of us will pay for it in the quickest manner possible so we can get down to the real work of solving the problem.

Sometimes that means credit card debt. Other times it’s payments that stretch out for years.

Neither of those options will help you get out of debt.

Having an emergency fund at the ready is a “no thinking necessary” solution to big problems that require all of your attention.

An Emergency Fund Is the Key To Getting Debt Free

An emergency fund is not a savings account that you raid when you need to make a big purchase or cover a few extra bills. T

his money should be set aside just for unexpected expenses you couldn’t have seen coming.

A broken bone. A car wreck. Getting laid off or asked to go on furlough.

These are true emergencies. An unexpected expense such as one of these would be the reason to dip into your emergency fund.

How Much Should I Save Before Paying Debt?

A common starting point is to set aside a $1,000 emergency fund before you tackle debt.

Any amount you can save is that much less you’ll owe at a crazy high interest rate. No amount of money in savings can compete with a credit card at 19% interest.

If you ever hope to really save money, you must get rid of credit card and high interest debt.

How To Get That Emergency Fund Together

Drop all your debt and bill payments down to the bare minimum. If you’ve been throwing extra at your debt to pay it off quickly, pay yourself first instead.

Are you spending an extra $2.64 on your mortgage payment to round it to an even number? (I know I’m not the only one!) Stop doing that for now. Put that little bit in savings, too.

If you have to take a side job or work from home job here and there, do it. Today. Your future self (the one too busy dealing with the emergency to get a side job) will thank you.

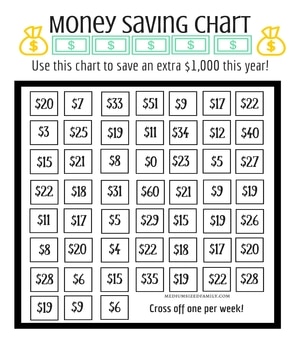

Make the job of saving money more like a game! Try my free money saving challenge that makes it easier to reach that $1,000 goal!

Get control over your unexpected expenses, and you’ll finally reach your goal of being debt free.

Jumping out of your car to find a flat tire will never be fun. But at least you won’t have to wonder how you’ll pay for it!

Here are 30 more ideas that will help you build that emergency fund!

How do you handle unexpected expenses?

My brother always tried to get my Mother to spend more in her later years. Coming from the depression era she always looked at him and said no way. She asked him are you going to buy me a new furnace when it breaks? She was so smart about her money.

Our emergency fund is a huge stress reliever. I don’t know what we would do without it sometimes. The important thing is not to touch it unless you absolutely have to!

It certainly helps you to sleep better at night when you have one!

Hello Jamie,

Thanks for sharing the tips. Hope it will help me a lot. And like the quote “Grandma told you to save up a rainy day fund.”

I do think some of the reason Dave gets flack for his emergency fund is that his number seems low. $1000 is a great start, and I think it’s fine for one person. But for 3 of us, it’s not enough to make us feel secure. We only have mortgage debt, but if we had more to pay down I think I’d still want our EF to be $1000 per person ($3000) before getting more aggressive.

That said, any EF is better than no EF. The unexpected always happens.

This is true, but even the $1,000 number is intimidating for many people (especially people just beginning their debt payoff journey!).

Very good reminder! We have been visited by Murphey way too many times this year! I’m ready for him to go on vacation! Emergency funds can be life savers!

Such a timely post! Our car was written off two weeks ago and although we will get some insurance money it will not pay for what the car was worth to us. Thank goodness we have emergency savings – I cannot emphasise how important this is.

Oh yes the emergency fund… Still working on that one 🙂

All of these at one point in time have contributed to more debt in our household. We had to start treating unexpected expenses as regularly occurring expenses before getting control of them.

#3 is so true for me!!! The unexpected expense is so upsetting and then everything else goes off the rails! I’m trying hard to stay focused and keep my head on straight. I’m also trying to view them as unWANTED expenses instead of unexpected because I have learned I need to expect them!