Paying bills online is great, because it’s simple and saves the cost of a stamp and an envelope.

But sometimes you want that special satisfaction of writing a check for the last payment on a loan. You can write something snappy in the memo box, like “So long, suckers!”

Trouble is, these days that satisfying final payment is far off and fleeting for most of us car owners.

We sign on to loans that last so long they might as well have a seat at the dinner table.

If you’re getting a loan for a car, you want to make sure you don’t sign your life away. It’s not as popular these days, but there is still a way to get it done. Let’s look at the problem and some solutions.

Before we get started, this post assumes a few things about you…

First, you don’t have cash to buy a car. (If you do, I’m flattered that you clicked here anyway! You might prefer this post about pantry challenges, though.)

You can’t, or won’t, follow the Dave Ramsey plan for starting with a $2,000 car and working your way up. (Personally, I think that car is going to cost you a ton in maintenance and repairs. But you might luck into a nice deal.)

You need a car. (You don’t have a lifestyle that supports biking or only borrowing a car occasionally.)

Is that you? Then let’s dive in.

The New Normal in Getting a Loan for a Car

Did you know that (according to this article) the average length of a new car loan these days is 67 months? And loans for even longer lengths (73 months and even 84 months) make up nearly 30% of all new car loans.

Used car loans aren’t much better. Many of them stretch beyond 5 years.

That implies that people are buying more car than they can honestly afford. It’s no wonder that auto loans topped $1 trillion this year.

Why are we paying more?

There are lots of reasons for this. The price of used cars is through the roof. When our family last shopped, we found car lots asking $10,000 for a car that already had 100,000 miles on it.

Who can afford to make payments on a car that’s almost sure to also have monthly repair bills?

If you want a deal on a vehicle, forget cash. Many dealers make their money by referring you to their banks. You’ll get your best deal by signing a loan at the best rate you can get.

Ideally, you’d sign for a loan with no early payment penalty and then pay it off as soon as possible. That said, don’t fool yourself into thinking you’ll pay it off early if you have a history of making minimum payments.

What’s the difference?

You probably know that you should pay on a car for the shortest time possible. But why?

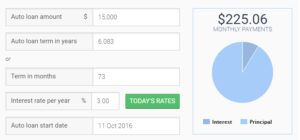

Watch what happens with a $15,000 car loan when you change the length.

(Screenshots from Bankrate’s auto loan calculator.)

5 Year Loan

This one looks ok. A 5-year loan like this will cost you $1,171.82 extra in interest.

73 Month Loan

73 Month Loan

This loan looks more affordable! Now you can get the car you wanted.

But hold on. A 73-month loan will cost you $1,429.05 in interest. Sure, you saved $44.47 per month, but it’s going to cost you $257.23 more to drive the same car.

Not to mention the extra 13 payments you’ll pay the bank instead of yourself.

3 Year Loan

A 3-year loan is cost prohibitive for many of us. If we’re shopping loans in the $250 range, we can’t swing $436.22 every month.

But the person who took this loan only pays $703 in interest. That’s a savings of $468.82 over the 5-year, or a whopping $726.05 savings over the 73-month loan!

How can we make the 3-year loan more realistic?

Look for ways to chop off $1,000 increments.

Begin by negotiating.

You know that you should never pay sticker price for a car, but some of us are too shy to ask. Take along someone more assertive if you need to.

Look for a car that is less than $15,000.

Another tip that sounds obvious. But on a car lot, it’s easy to start justifying. Car A has a couple of awesome features that Car B doesn’t have.

When you’re already spending $14,000, what’s another $1,000?

Well, it’s a lot! Step back and think of how long it would take you to save up that kind of money.

Sacrifice a 4 door for a 2 door. Give up heated seats or the moon roof. It’s worth it to bring your loan down to 3 years. With fewer payments, you’ll be able to pocket the savings and get the car you really want next time.

Negotiate on price, not payments.

Use a good car loan calculator. This one allows you to include the often forgotten cost of taxes. Don’t forget that the dealer will also charge you extra fees (look up how much your state allows them to charge).

While you’re playing with that calculator to find out what price is actually in your affordable range, notice something. Adding a few hundred dollars to the cost of the car only wiggles your monthly payment by a few dollars.

So when the salesman squeezes you to just pay them $5 more per month, you’re actually giving them a lot more for the car than you realize.

Go in armed with the right information, knowing exactly how much money you want to pay for the car, accounting for taxes, title and other fees.

Save up a down payment.

Getting a car with no down payment is popular, but it’s costly. Every $1,000 you put down will save another $30 off of your monthly payment.

Ideally, you’ll be saving up monthly payments for a bit before you buy the car. If you can’t afford to save the cost of the monthly payments beforehand, how will you afford the payments later?

Sell your old car yourself.

You’ll get more money out of your old car by selling it on Facebook or Craigslist rather than trading it in at the dealership. That’s more money you can put down on your loan.

Check out “How can I sell stuff online locally at the best price?”

[et_bloom_inline optin_id=optin_10][et_bloom_inline optin_id=optin_8]

Other ways to lower payments.

Broaden your horizons.

Examine all of your options. Be sure to look at all brands. It pays to be loyal, but all of that pay goes to the company (not you).

Shop private sales.

Private sales are nearly always cheaper than dealer prices.

Consider timing.

When buying from a dealer, you might have heard that buying later in the day, month, or quarter will net a better deal. But I’ve been told that this simply isn’t true. You’ll get the same deal whenever you shop, so don’t sweat your timing too much.

Buying from a private seller? You might find them more motivated to sell at Christmastime, but greedier during tax return season.

Remember these tips any time you’re getting a loan for a car.

Choose a shorter term, and bank the rest of the payments yourself. Soon, you’ll have a sweet savings account set up for your next car. Now tick down the days until your last payment, and start planning that memo line zinger.

The best part about keeping car payments down is that your budget will thank you for years to come.

And those “so long suckers!” checks will come a lot sooner!

Other debt got you down? Learn how we knocked out tens of thousands in credit card debt, all while raising 5 kids on one income!

Do you avoid car payments at all costs? Or are they a necessary evil?

I never buy a new car. Immediate loss and not a good financial decision. 2-3 years old is good enough and half the price. and you get more options on a used car than you get with the new ones. unless I hit the lottery (and maybe even if I do) I’ll not ever ever buy a new car or finance anything for longer than 48-60 months.

This is incredibly awesome advice! Advice that I’ll be sure to heed the next time we’re on a car hunt for sure!

Wow, thanks! I appreciate that, and glad you found it helpful. 🙂

I especially would not want a long term loan on a much used car….which is about what you can get for $15,000 right now. Cars are expensive. Fortunately, they last longer too, at least with good care. My best bet is to take care of the car I have so i can avoid a new car purchase as long as possible!

I totally agree with that! We try to be quick to pay them off, and then make them last.

These are such great tips! Thanks for sharing!

I never knew these things. Thanks for sharing your knowledge.

We have a car loan, but thanks to keeping our credit scores high, our interest rate is less than 2%. We decided to buy an inexpensive new car when we transitioned from 2 cars down to 1. But I think in the future I would look at a 2-3 year old car rather than new. Ideally you can get away without a car loan at all, but you’ve given us lots of great advice to try to reduce a loan.

We were able to find a 2 year old car with low miles for under $15,000 the last time we shopped. It takes some careful shopping, but you can find a good deal on a slightly used car. Even better when you can get away with being a one car household!

I agree with your points.

We have one paid-off car, and one almost-paid-off car. Cars are purely utilitarian to me, so that helps keep costs down. 🙂 I want a vehicle that’s reliable, safe, and fuel-efficient, and used cars feel like a much better deal to me. (Let someone else pay for the depreciation!) Both of our cars are in good shape, so we should be able to get a year or more without payments, once the second one is paid off. (I hope I didn’t just jinx myself…)

Totally agree! I want a car that will get my family from point A to point B. As long as it’s reliable and doesn’t cost a fortune to keep on the road, that’s the car for me!

I have car payments and I hate hate hate hate hate them! 🙁 I just wrote that darn check today! Wish I could write “so long suckers!” lol 🙂

This is really awesome advice (that actually made sense to me – so excellent job writing it lady!) and I’m saving it for later! 🙂

So glad it’s helpful! I always love the advice that you should pay cash for cars…but it’s just not realistic for most of us. Hopefully we’ll get there eventually!

Once you do write that satisfying memo line, keep up the payments–to yourself for the next car fund. We did it for about 8 years. Last year we used that (plus some money we “borrowed” from our other savings) to pay cash. I’d rather pay myself that interest than the bank. I’m not sure we’ll be able to manage that next time we need a new vehicle, but it sure was nice this time!

What a great post! Honestly, I always let my hubby handle the car stuff but I feel so much more informed now! Thanks so much for sharing with us at Share The Wealth Sunday!

I’m always excited about helping out my readers, so this makes me very happy to read. 🙂

Keep your credit score high and join a credit union. We just financed $10,000 towards a $20,000 purchase price on a 1 year old car. Interest rate was 1.45% for three years. Financing cost is under $300. My bank wanted a $150 doc prep fee and 5%, so shopping around for financing helps.