Paying down debt can be a long, hard road. Make it easier with some simple tricks. You’ll be surprised what happens when you break up your paycheck!

You’re paying down debt, chugging along and happy that you got your balance down a bit. Hooray!!

And then?

…you find a surprise bill in the mailbox.

Ugh.

You don’t have money to cover the bill, so… you pay it using your credit card. Now the card balance is nearly as bad as it was before.

And you’re right back where you started…trying to get that balance down again.

It’s so frustrating!

Especially when you’ve been trying so hard. You skipped happy hour with your buddies. You cancelled your cable service.

Now it feels like all that sacrifice has gone to waste.

Paying Off Debt Is Frustrating

Most Americans are in the same boat as you. We’ve all heard the stats. The average American owes $15,000 just in credit card debt.

It’s a pretty common problem that lacks an easy solution. Otherwise, everyone would be out of debt tomorrow.

Still, there are some steps you can take to simplify the process a bit.

Our own family has a big goal to pay off debt this year. It’s our #yearofno. But that hashtag motto isn’t the only tool we’re using to wage war against credit cards that have taken over too much of our lives.

[et_bloom_inline optin_id=”optin_8″]

I’m going to share another way we’re gaining ground in our debt battle with you today.

How to Get Out of Debt By Breaking Up Your Paycheck

Step One: How To Use Your Regular Checking Account

Here comes the b-word, and I hope you expected to see it here: budget. You’ve got to start with one! It’s the only way to get control over your money.

If making a budget never seems to work out, there’s a good chance that the problem is with the type of budget you’ve been using.

Trying to make a monthly budget work when you get paid every other week is like trying to use a squishy toy to fill in the blank spots on the puzzle you’ve been working on.

I mean, you might be able to make it work…but it ain’t gonna be pretty.

Instead, try this budget planner that’s built for real, messy lives.

Step Two: The Other Accounts

Your checking account covers your every day bills.

But here’s the trick… don’t deposit your entire paycheck into that account.

You’ve got irregular bills and expenses, too. So let’s pay those in the laziest way possible.

I’m serious. Human beings are a lot like water. We’re basically on a mission to follow the path of least resistance.

The good news is that you can use that to your advantage.

How To Use Laziness to Your Advantage

Automate as much as possible. Set it up once and then let it go.

(Ok, don’t actually forget about it. Look at it occasionally to make sure it’s doing what it’s supposed to do.)

[et_bloom_inline optin_id=”optin_8″]

Automate Retirement

Yeah, yeah. You’re supposed to save for retirement. In fact, you should have started years ago.

Well, don’t let that stop you from starting now.

The fact is that you’ll never have the money to save if you don’t make it the most important thing.

So unless you’ve already cut all your frivolous spending and still have no money left each month, you need to set this up now.

Start by saving just 1% of your paycheck towards retirement if you’re nervous about it.

(Remember that this comes out of your paycheck before you pay any taxes. So you won’t even be missing the entire 1%.)

And if your employee offers a match, you’re passing up free money! Only a crazy person would do that.

Automate Healthcare

If you have a family, you probably have medical bills.

These days, lots of us have HSAs. Just make sure you have enough in there to cover all of those deductibles.

If you don’t have an HSA, set up a FSA to cover those unexpected expenses.

Believe me, you’ll thank yourself when you’re suddenly spending an evening in the ER. You have enough on your mind without wondering how you’ll pay for it, too.

The Debt Destroying Account

If you’re ready to make debt payment a priority, here’s a secret tip that made a HUGE difference for us: open a separate checking account.

We use Chase bank for checking, and love how easy it is to do most of our banking online.

Once you have your new bank account, file direct deposit paperwork at work so part of every paycheck gets funneled right into your new account.

How much can you comfortably pay towards debt? (For us, it was 15% of each paycheck.) Chose an amount and get started already!

Then, every pay period, pay your credit card bills (or whatever debt you’re tackling) from this new account.

There’s something about keeping this money separated from all of your daily spending that helps you mentally keep it out of your budget.

Plus, let’s face it…if you make it difficult to get to that money, you’ll be much less likely to blow it on something stupid.

(Definitely do NOT get a debit card for this account! If you have to have one, freeze it in a huge block of ice or give it to your Mom to hold on to.)

Use your laziness to your advantage!

Other Accounts

That separate account for paying off debt worked miracles.

So I got to wondering how else we could use this idea.

You know, like covering the huge bill that always comes with filling our big propane tank.

Even though it happens every winter, we never seem to be ready for it.

So we opened ANOTHER savings account that I called “Heat Bill”. I set up an automatic withdrawal from our checking account that will deposit into this account every month.

It’s lazy-proof.

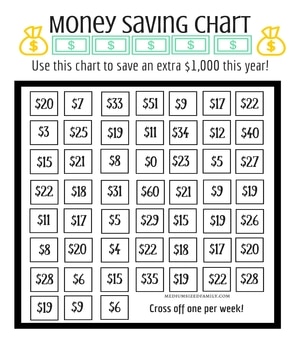

This idea is actually called “sinking funds” and you can do a ton with them. Get more ideas here.

“Extra” Paychecks

Hubby gets paid biweekly. Twice a year we have a month with an “extra” paycheck.

But it always annoys me when people talk about this paycheck like it’s free and clear money. Because that’s not entirely true.

The family still wants food, the gas tank still runs empty, and the expenses don’t stop coming just because it’s “extra paycheck time.”

(Want to know how I keep our grocery bill for 8 people under $800 per month?)

That said, you SHOULD still have some extra money from this “extra” paycheck.

Figure out how to put it to work for YOU. Maybe it can cover irregular bills like semi-annual insurance payments or even something FUN (like a vacation!).

If you’re paying down debt, break up your paychecks and take the lazy way out!

What a sigh of relief you’ll heave when a bill comes in and you have money at the ready to pay. No more relying on credit cards for you!

Ah, the good “free paycheck” – I fell into thinking that for a bit, then realized that, no, it’s not, because I still needed food and things to cover those two weeks, ha.

I would be curious, though, as to how you feel about Ally and Capital One 360 – I’ve heard great things, and then googled for reviews and found some horrendously scathing ones. Granted, I’m sure only the people who are peeved are searching for these complaint sites (to then also complain on) but a lot of people there said they were all of a sudden locked out an account or their money was taken from them because of miscommunication or random fees they didn’t know they would get. I’d like to set up an account like this (a savings account with no fee, and no worries of having to keep a certain amount in it, unlike how it is with my actual bank) but don’t want to deal with it all of a sudden no longer working.

When I was working and living with my mom, though, I did the split up the paycheck thing. I paid half of my portion of the rent with my first check, and the other half with the second check. It was much easier than having one check a month that didn’t have anything come out of it, only to end up with most of the second check gone as soon as I got hold of it!

We have been with Capital One 360 since they were ING Direct. So it’s been several years. I have had trouble with my account a time or two (which wasn’t there fault..in one instance I had sent a payment to the wrong account) and they have helped me through it. I have absolutely no complaints about them.

We’ve been with Ally for a year or two, and have had no trouble with them so far, either.

I can’t promise you’d never have trouble with them, but I can say that my own experience with both banks has been great.

Woo, thanks! Like I said, the bad reviews were on the kind of sites people have to go to find complaints, and then take the time to write, so more than likely *just* angry people are going to be there, for the most part, but all the reviews I’ve read online just cover what they do and how the writer has set up an account, etc, not that they’ve been using it for x-amount of time and did this or that with it.

I used You Need A Budget (YNAB) before I got married and loved it. (Now my husband ussd his super awesome spreadsheet for our budget.) About the month ahead concept: it takes awhile to get saved up to that point, but it is awesome. We are going to try to do it once our collective debt is paid off next summer. It is straightforward of you have a regular weekly or biweekly paycheck – budget all your regular expenses, including the amount you want to save, or “roll over” to the next month. Continue until you have a month’s worth of expenses saved away, in your checking account. This is where the YNAB software shines, as it automatically does this for you, and helps you visualize all that extra as your cushion, rather than awesome free play money (ahem.) Hope this is helpful!

Yes, that is helpful! We’re super interested in trying it, but have decided to put trying it out on hold in the #yearofno. Maybe next year we’ll give it a shot.

You always have the best advice. We are trying to live a debt free life right now. It is hard work but it can be done.

You made my day! Thanks for your sweet comment. It really is hard work, but so worth it.

Ah the ‘extra’ paycheque… it’s such a mind trip! We currently pay our mortgage biweekly so it always seemed so disappointing when this ‘extra’ money would disappear.

We use YNAB and I absolutely love it. We used a cash envelope system for many years but I felt like it meeting our needs in terms of tracking the money spent. I also like to divide things into sinking funds and I found YNAB was the best way to do that while keeping the money in one spot instead of many accounts. I also love the living on last months income part- it’s been a major stress reducer for us.

We have YNAB 4 which is a one time fee. I did a full review of it here: http://onemamatoanother.com/you-need-a-budget-ynab-software-review/

Excellent! Thanks for sharing.

I love getting those “extra paychecks”! Such wonderful advice on how to use them. Thanks!

All these are very helpful ideas to save money.Hope you will reach your goals..

We use the same system, but it never occurred to me to use are extra bi-weekly check to pay our auto insurance in full – that’s genius! And it would be one less bill to avoid. I think the next one we get is later on this year and I’m going to use it and finish paying off our premium. Hopefully, that will allow us to catch up before the next premium is due and receive that discount. Thanks for sharing this with us, you think your system is working fine and then you learn something new!

I’m so glad I could spark a little inspiration for you! I see I’m not the only one who hates monthly bills. 😉

Great advice. I really need to do more of this. My family has hit rough times the past few years and we’re just starting to come out of it. We opened a 2nd bank account but I think the idea of a 3rd account specifically for debt payments sounds great.

I hope it’s as helpful for you as it has been for us. Good luck on your debt payoff journey!

This is brilliant. I never thought about breaking up my paycheck to take care of certain things through each account. We don’t have any credit card debt at this point but the medical debt that we have and the co-pays are killing us. We definitely need to look into the medical savings FSA. This could really save us some money. Thank you for always coming up with great ideas and for sharing them so that we all can get to a good financial status.

I hope that it’s helpful for you! The last thing you should have to worry about at a time like that is medical bills.

Some great tips here! Luckily I don’t have any credit card debt, but I’ve been stuck in my bank overdraft for years. My goal is to get out of it so I’m not constantly paying interest on it.

Thanks so much for sharing over at #FridayFrivolity

Such wise advice Jamie! We’re neighbors today at Life is Lovely! Happy to connect with yoU!

Such great tips! I especially like the idea of setting up a separate account for your debt payments. Thanks for sharing at Friday Funday Blog Hop 🙂

That’s been a really big part of our strategy, and I’m not sure that we’d be nearly as successful in paying off debt without it.

Awesome advice! We do this too and it saves us so much and we are debt free except for our mortgage! Thanks for sharing at #lifeislovely

Love these tips!! So smart, especially about your laziness work for you…! Featuring you today at #FridayFrivolity!! 🙂

I needed this, thank you so much for these steps. I’ve been struggling with a credit card debt since last year and its killing me. I feel like I’m getting no where with it. I’m hoping this will help me a lot. So glad I came across your post on #WayWow

Our family is battling our way out of credit card debt this year, too. There’s lots of info here about how we’re getting out of debt. So happy I could help you out!

Great tips thanks for sharing with Hearth and soul blog hop.

I spreadsheet, but on paper. I divide each check into about 20 categories. (Water, gas, electricity, car gas, entertainment, vacation, repairs, church, drivers ed, insurance, gas, groceries, home improvement, savings, gifts, etc). I take the amount needed for the year and divide it by 26….for each paycheck. There are no external checks. Each payday a certain amount goes into each category. Monthly bills are multiplied by 12 then divided by 26. Other amounts are estimated, like repairs, figure $1000 so $38 goes in each time. It’s all in a savings account. I transfer the amount needed based on bills into my checking account. I adjust the amounts a couple times a year, based on budgeted amounts for gas and electricity and if I discover other accounts that are needed, like drivers ed or graduation which I just created. $3 goes into each of those 26 times a year to hopefully have enough when my kids are there.

This is a neat idea. I especially like putting $3 in for misc. expenses. It’s small so it won’t hurt as much as paying that larger bill when it rolls in.

This is what I do too, but without the extra bank account because my office doesn’t offer direct deposit. So I spend about 45 min-an hour every quarter reviewing my spending plan and debt payoff strategy, and then auto-scheduling payments to come out of my account the day after every pay day (when the check clears). Then it’s like I never even had the money and the bi-weekly payments make me feel like I’m making progress!

That’s a really smart way to handle it! I like to batch jobs like that, too. It’s a relief to just have it done.

Awesome advice! Getting out of debt can be a nightmare but with the right software and money management it is totally possible. Thank you for sharing this advice!